In 2015, an estimated 54 million Americans were actively participating in a 401(k) plan at work. However, according to a 2014 study by Aon Hewett, only 15% had rebalanced their 401(k). Why does this matter? As the market goes up and down, the funds you’ve selected for your 401(k) will change in value, but not equally. Rebalancing is the process of periodically realigning your account so it more closely resembles the desired investment style and objective. When you don’t rebalance, you lose control over how you’re invested.

Old 401(k) plans are poised to be forgotten

When saving for your long-term goals, it can be helpful to automate your monthly contributions, or “set it and forget it.” When saving for a distant goal, investors should try not to compulsively check their accounts, fretting over the impact of daily headlines and panicking when the market inevitably has a downturn.

Although it’s good to stay focused on your long-term goals and not get too wrapped up in the daily gains or losses in your account, that doesn’t mean you should put your investments out of your mind completely. This is especially true for old 401(k) plans still with a previous employer or an old plan that you have rolled over into an IRA. These accounts are much more likely to be neglected over time.

The value of being diversified

The value of being diversified

The value of being diversified

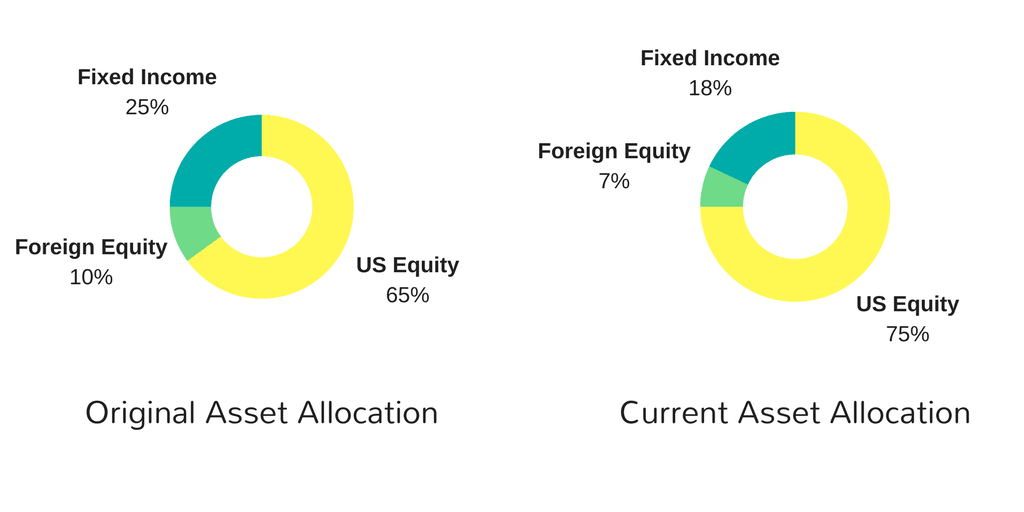

The value of being diversifiedWhen you choose the funds your 401(k) contributions will be invested in, you’re setting the asset allocation for the account. An asset allocation should always be aligned with your risk profile, which typically will depend on a number of factors, such as your age and the number of years before you retire. If done correctly, this asset mix, (often represented as a pie chart), can help mitigate the risk of incurring sharp losses because each “slice” of the pie is expected to perform differently under various market conditions. This is the idea behind diversification.

Let’s assume you’ve set your asset allocation to be 70% stock funds and 30% bond funds, which is aligned with how much risk you are comfortable taking. When you check your account one year later, you see that the stock funds are now 90% of your portfolio. If you don’t rebalance your portfolio to get back to the 70/30 mix, you may be more exposed than you realize during market volatility.

The goal of a diversified portfolio is to gain exposure to various asset classes in the market while limiting the concentration risk that comes with being over-exposed to one specific class, such as real estate or international equity. If you don’t rebalance your 401(k), your portfolio is likely to become less and less diversified over time, which could end up costing you.

How to rebalance your portfolio

Generally, you may only need to rebalance your portfolio once or twice a year, and sometimes, perhaps not at all. The first step is to compare your current asset allocation (which in our overly-simplistic example is 90% stocks and 10% bonds) to the intended asset mix, which is 70% and 30%, respectively.

Since there is a meaningful gap in the actual versus intended mix, it may be time to rebalance. To restore the account to the initial allocation, you will need to sell off a portion of the out-performing equity funds and reinvest those dollars into the bond funds.

It may seem counter-intuitive to sell an asset that has been outperforming, but remember: past performance does not indicate future results. During a market correction, the lack of diversification in the portfolio exposes investors to much more risk than they likely expect.

How Often Should You Rebalance Your 401(k)?

Rebalancing During Market Volatility

Important considerations

When you rebalance a tax-deferred account like a 401(k), there won’t be any tax consequences. However, if you have your own taxable brokerage account, rebalancing becomes much more complex. Further, there may be other costs involved, such as trading fees.

Before you rebalance your portfolio to mirror its original state, make sure your initial asset mix was appropriate in the first place. Do-it-yourself investors are often flying high when the market is up, but when it goes down (and eventually, it always goes down), they decide to enlist the help of a professional. Maintaining a diversified portfolio that is aligned with your changing goals is a necessary and ongoing process. Unfortunately, many busy professionals end up falling short as they often lack the time, or interest, in becoming an expert.