There’s a lot we know about the current state of the stock market, but we can only make an educated guess as to where the economy goes from here. Both are sobering to think about. As of the writing of this article, we have descended into the fastest bear market in history: it took only 16 trading days for the S&P 500 to fall 20% from recent highs.

So what does all this mean for individual investors saving for retirement, college, or just because they can? Should they change course knowing where this train is heading?

As of the writing of this article, the index is down over 30%. While the more telling unemployment numbers won’t begin to roll in for a few more weeks, we know the U.S. economy is almost certainly heading for a recession. In fact, we’ll probably learn later that we’re already in one.

If you’re a quarantined—but employed—investor, you might be wondering whether you should keep investing despite these sobering facts. While the unmitigated selloffs in the stock market recently may not have exactly inspired confidence, you need to remember that you’re investing for the long haul. There’s perhaps no worse place for short-term money than the stock market.

A quick history lesson on recessions

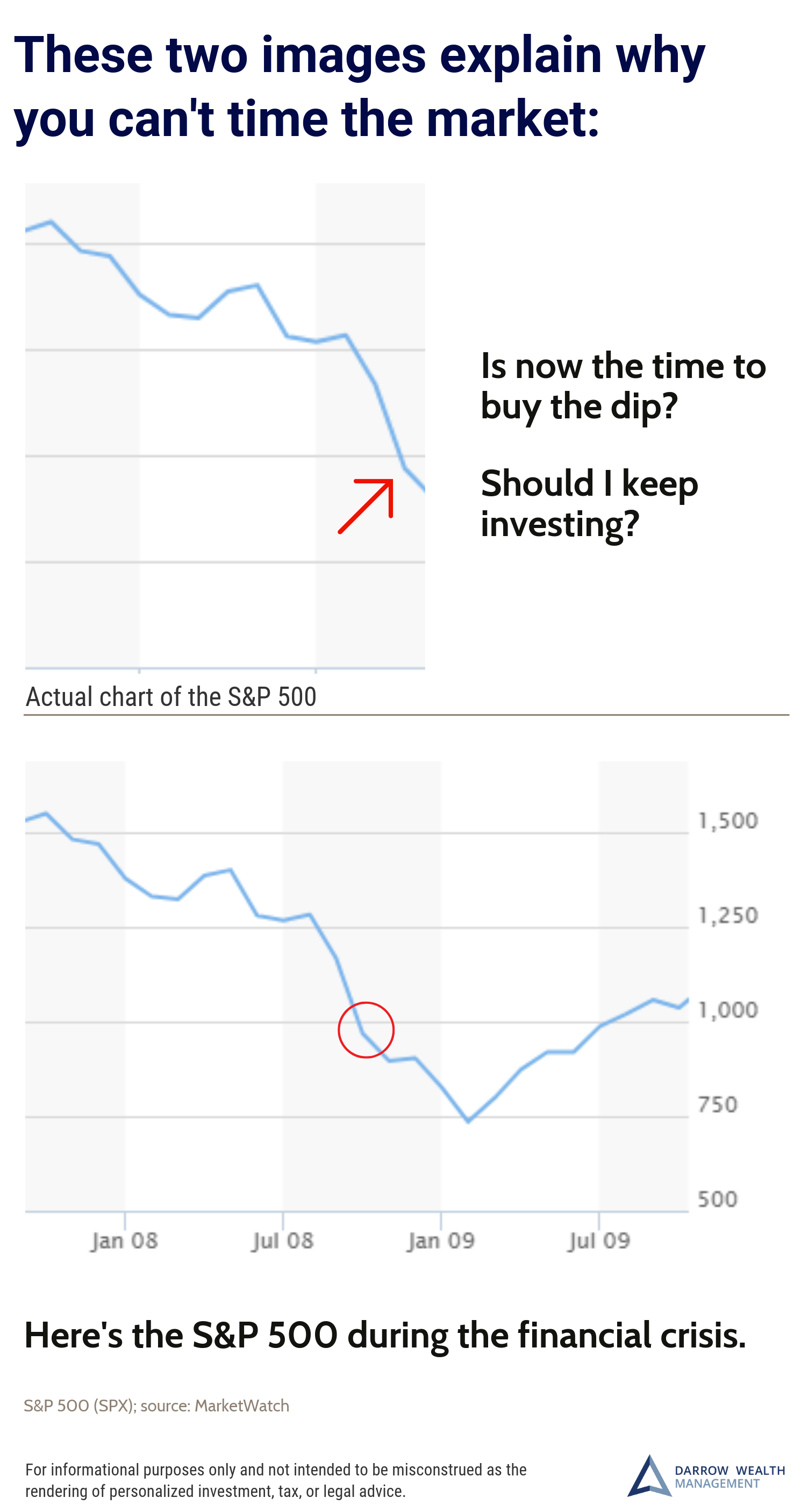

The last recession was the 2008 – 2009 financial crisis. Even though the coronavirus outbreak is expected to put the U.S. in another recession, the reasons for the two downturns are VERY different. In short: this is not 2008. Though the current situation is expected to be painful for a shorter period of time, in some ways it may also be more severe. It will certainly be more abrupt; that we already know.

During the financial crisis, the U.S. was in a recession for 17 months (a recession is defined as two or more periods of negative GDP growth). During that time, the S&P 500 lost over 56%. The financial crisis in 2008 was no ordinary recession—it is commonly called “The Great Recession” and was the worst economic crisis since The Great Depression.

Every recession and economic downturn is different: losses in the stock market, length and severity, and the unemployment rate will all vary as the circumstances of each event aren’t the same.

But there is one really important thing that ALL recessions have in common: they end. They all eventually end.

How to invest during a recession or market downturn

The U.S. has not officially entered a recession though the possibility seems very likely. During times like this, it’s usually best not to look at your retirement accounts. Unless you’re nearing retirement, that money is for the LONG term.

Most of us aren’t just investing for retirement, though. A brokerage account is the only type of non-retirement investment account and it’s also a great way to build wealth and bridge the gap to an early retirement.

So if you have extra cash in your bank account, you might be wondering whether it’s a good time to put money in the stock market…or perhaps you’re second-guessing regularly scheduled contributions to your brokerage account.

First off, your personal circumstances dictate when it’s a good time to invest, not whatever is going on in the stock market at the moment. This deserves special consideration right now, as investors with otherwise stable employment may now need to prepare for an unexpected job loss.

Second, even if you bought ETFs at some of the pre-financial crisis highs, you’d be better off staying invested than if you sold before the bottom and got back in during the recovery.

Keep in mind, during especially turbulent times, there isn’t always somewhere to hide. So while diversification is the best way to achieve risk-adjusted returns, it doesn’t mean you won’t lose money.

Typically, stocks and bonds move in opposite directions which can provide safety for investors who have fixed income allocations. As we’ve seen in the last few weeks—it doesn’t always work that way.

Sitting back and waiting for clear signs of the bottom or the recovery in an attempt to outsmart the market is a fool’s errand. It just doesn’t work that way.

No one knows where the bottom will be during the coronavirus crisis and the only way to know when we’ve turned the corner is after it happens when we look back at the data and pinpoint the moment things finally began to turn around.

Here’s the good news, though: things will get better eventually and if you have cash to invest and the time to let it move through the ups and downs, then you don’t even need to try and predict the bottom to come out on top. It’s about time in the market—not timing the market.

Related:

Analysis: How Market Volatility and Cash Flows Impact Your Account